Your Cost Behavior Patterns Will Shock You!! An Illustrative Guide

Before studying cost behavior, a manager must first comprehend the critical business activities that may impact costs. Then, management can usually specify activity levels in dollars, units, and other metrics. Furthermore, the administration should attempt to establish a link between activity levels and costs.

However, not all costs can change as a result of business activity. So, despite a change in economic activity, some expenses may remain unchanged. For example, a company must pay insurance whether or not it is in operation. In addition, some costs do not fluctuate in lockstep with changes in business operations. Generally, we use mathematical cost functions to study the organizational first behavior. So, let’s focus on each type of cost behavior. We will also study how each cost behavior function works.

What Is Cost Behavior?

The way that a company and its operating expenses shift or remain consistent over a certain period is cost behavior definition. Now, Patterns might shift, especially as the company’s production or sales volume fluctuates.

The range of sales or output based on which cost behavior patterns do not change is called the relevant range. That’s why there are three types of cost behavior patterns such as fixed cost, variable cost, and mixed cost.

What Are Different Types Of Cost Behaviour Patterns?

Any discussion of cost behavior should begin with the notion that most costs can be classified as fixed, variable, or mixed. There are also hybrid cost behaviors that don’t fit into one of these three categories because they are used in more complex accounting programs. So, understanding if a cost is a fixed cost or a variable cost is the most important because they are the cornerstone of all other cost behavior patterns.

Fixed Cost

Fixed costs exist independent of the number of production or revenue generated by the company. Rent, insurance, and loan payments are examples of fixed costs. Property taxes, depreciation on equipment, and non-consumption services such as Internet access are also other examples of fixed costs.

As production increases, the fixed cost per unit decreases, but it keeps the fixed cost constant. So, certain fixed costs may fluctuate depending on business activities. For example, if a company introduces a new product, its promotional expenses may rise over regular levels. But, only the company management is responsible for changing the discretionary fixed cost.

How To Calculate Fixed Cost?

Total production costs — (Variable cost per unit × Number of units produced) = Fixed Cost.

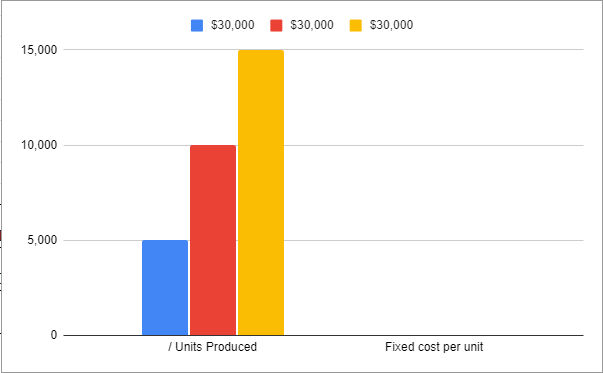

For example, a company has a total fixed cost of $30,000 for its production purpose. If they change the production per unit volume to 5,000, 10,000, and 15,000 per year, it will change the fixed cost per unit. However, the total fixed cost will remain unchanged.

| Financial Years | Year 1 | Year 2 | Year 3 |

| Total Fixed Cost | $30,000 | $30,000 | $30,000 |

| / Units Produced | 5,000 | 10,000 | 15,000 |

| Fixed cost per unit | $6.00 | $3.00 | $2.00 |

Variable Cost

The totals of variable costs will alter depending on the degree of activity in the company. For example, the cost of direct materials and labor corresponding to production levels in a manufacturing process are variable cost behaviors. If you want to increase production, you’ll need more resources, machinery hours, more labor, and vice versa.

In the same way, the variable costs in a business entity will vary depending on the goods and equipment necessary and required travel charges and support people labor costs. For a tradesman, commission fees, shipping charges, and inventory management costs are some examples of variable costs. In addition, as production increases, variable costs per unit also increase.

How To Calculate Fixed Cost?

Cost Per Unit x Total Number of Units = Total Variable Costs.

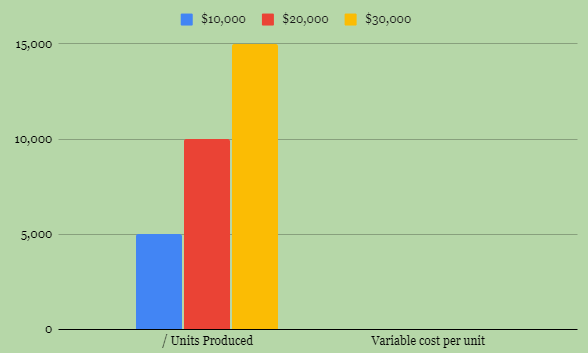

For example, a company spends $10,000, $20,000, and $30,000 every year to buy the raw materials for its production. As they change the raw material purchase cost, their per production unit volume also changes. It shows how a variable cost can change if the business activity changes, but the per-unit cost stays constant.

| Financial Years | Year 1 | Year 2 | Year 3 |

| Total Variable Cost | $10,000 | $20,000 | $30,000 |

| / Units Produced | 5,000 | 10,000 | 15,000 |

| Variable cost per unit | $2.00 | $2.00 | $2.00 |

Mixed Cost

Fixed and variable costs have traits in common with mixed costs. Therefore, a cost that includes both fixed and variable cost components is called a mixed cost. For example, assume the monthly utility bill includes water, electricity consumption, fixed-rate limits for gas, and additional penalties if those limits are exceeded.

The costs are fixed during periods of low activity when the business does not reach flat-rate levels. However, consumption rises above the flat rate during periods of high output or sales, and overall expenses fluctuate.

Fixed vs. variable cost

The fixed cost is an unwavering component. It will not change in the short term. The business might go through variations. However, the fixed price will remain the same.

The fixed cost for merchandising or rent, salary of managers and executives, insurance, etc. Similarly, the fixed price in manufacturing or taxes, equipment leasing expenses, and insurance costs.

We discussed that fixed costs remain static. It does not change with any change of activity. But what about the person unit fixed costs?

We will take the example of a T-shirt printing company here. The owner has a fixed cost of 1000 as rent. He cannot ignore this cost even if he does not sell a monthly t-shirt.

Now, he can consider this fixed cost as per unit. Let’s imagine he manufactured 200 T-shirts in a month. So, he has to sell each of them at $5 extra. It will help him to recover the cost of monthly rent.

But the status changes when he sells 400 T-shirts instead of 200. The average rent cost he needs to recover from each T-shirt comes down to $2.50 when selling 400 pieces. The same comes to $1.67 when he sells 600 pieces each month.

With each piece unsold, he will keep going distance from recovering the monthly rent paid. But the effect will be lesser when he manufactures more pieces.

The information highlights that despite the fixed cost of the rent, the level of activity impacts the unit fixed prices here. When activity is higher, the fixed price is lower.

Type variations

There are two kinds of fixed costs. We call them committed and discretionary costs. Generally, the differences don’t account for at the ground level. However, managerial accounting needs to segregate these two kinds of fixed costs.

Committed cost cannot be ignored if the company wants to function for example, the cost of leasing factory equipment. However, the discretionary cost can vary. For example, training costs.

You need to bear the cost only when new joiners join your team.

Variable cost

It is another fundamental cost classification. This cost varies based on the activity level of your business. For example, the cost of raw materials varies from time to time. The overhead cost and labor cost also change according to activity.

If you want to manufacture 200 pieces a month and involve 20 laborers for the same, the labor cost would be average. When the pressure rises to 2000 pieces a month, you must pay more labor costs. This is an appropriate example of variable cost.

Kind of variable cost

An example of variable cost in merchandising would be the hourly salary paid to sales staff hired on a project basis. In the case of manufacturing, the variable cost is the direct materials used to manufacture 1 unit of product.

Why Should You Understand Cost Behaviour Patterns?

Depending on how they will use the cost information, different firms use the term cost in different ways in management accounting. Different judgments necessitate different cost classifications. Let’s learn about the benefits of cost behavior patterns;

- Recognizing and comprehending cost behavior patterns has various applications within a business. It enables management to budget appropriately, lowering expenses and increasing revenues.

- Management and financial planners can create realistic production and sales goals by understanding the company’s cost behavior patterns.

- Furthermore, knowing a pattern allows management to determine the company’s break-even point and modify pricing tactics as needed. Management can also use the data derived from cost-behavior patterns to boost production, start new product development, or launch new services.

- A manager may want cost data to prepare for the following year or make judgments about whether or not to discontinue a product.

- In practice, as the utilization of cost data evolves, so does the classification of costs. For example, a single cost can be characterized as a fixed cost by one company, a committed cost by another, and even a period cost by yet another. So, if you need to understand Managerial Accounting, you’ll need to understand different categories of cost behaviors and how certain costs can be employed in various ways.

FAQs

People may still confuse fixed with variable costs. So, I felt answering these persistent queries is important:

Ans: Cost behavior is the change in the usual behavior of cost due to changes in operating hours or business activities. For example, the electricity cost will increase if a company increases its working hours. But, certain costs also remain unchanged despite the changes in business activities.

Ans: A business management studies cost behavior because it wants to understand how their operating costs fluctuate if they change business activities. Some of the examples of business costs are direct labor, direct material, overhead cost, etc.

Ans: If you want to define cost behavior patterns, you simply have to understand how business expenses remain intact or change corresponding to the changes in business activities. If there are varying production levels or sales volume in a company, that may change the cost behavior pattern

Sum It Up

As we have mentioned before, cost behavior patterns are an essential phenomenon in management accounting. If you understand the concept of cost behavior well, you can exercise better control over your company’s expenditures. So, if you want to know more about it, you can ask us in the comment section below. We will surely get back to you with an answer.

More Resources: